Investment expertise

Credit strategies

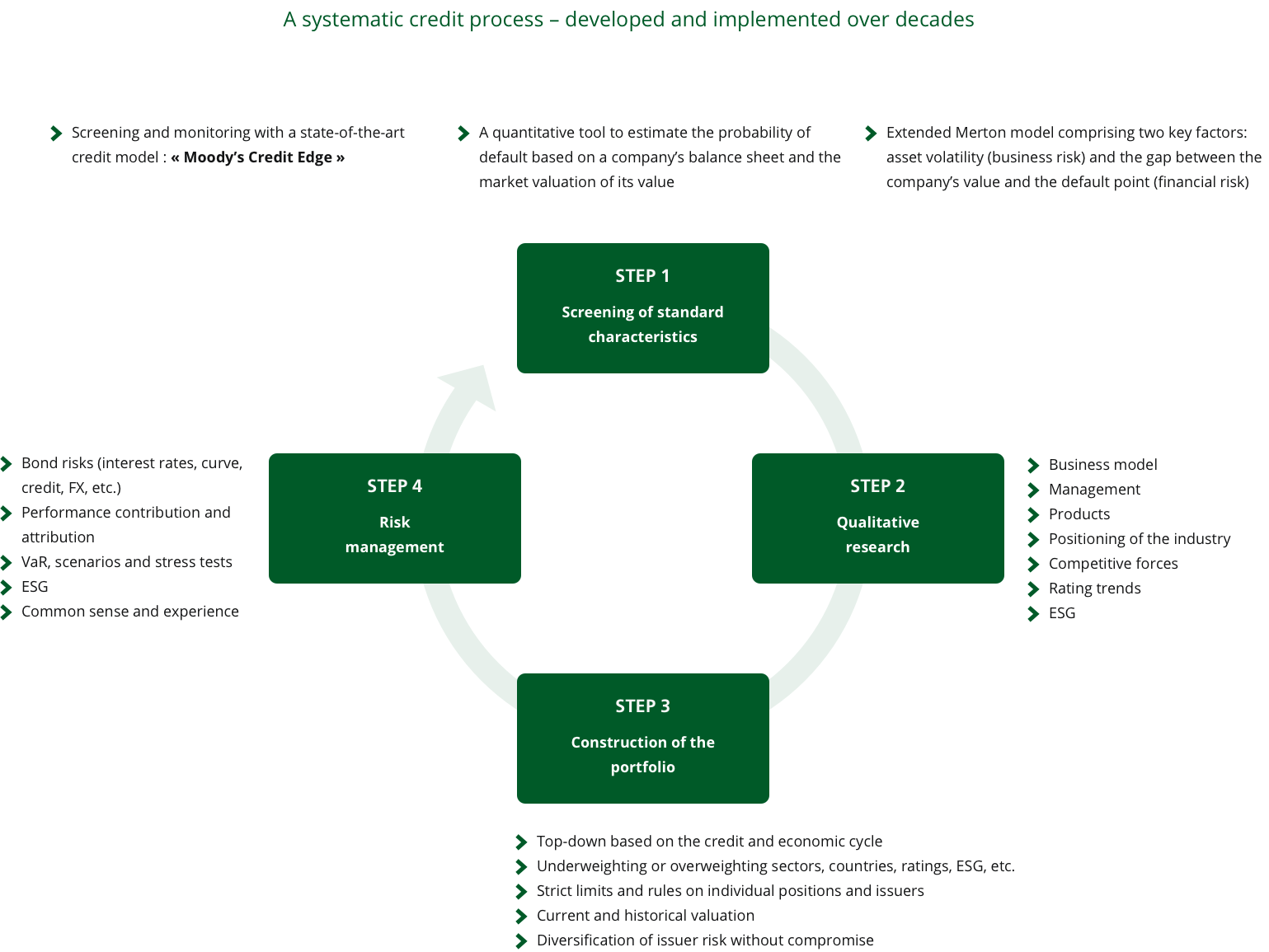

Our disciplined credit process is based on a quantitative and qualitative approach and has been developed and implemented over several decades, with no compromises in terms of diversification

Credit strategies

Step 1 – Avoid defaults, the basis for credit selection

What we do:

Due to the asymmetric profit/loss potential of assets with credit risk and the difficulty of offsetting bad investment decisions with good ones (unlike with equities), the top investment priority is the negative selection of fundamentally poor quality debtors.

We analyse and screen the entire corporate bond universe as well as existing portfolios using one of the best credit models, “Credit Edge” from Moody’s Analytics. This quantitative approach systematically covers fundamental analysis (balance sheet, financial risk) as well as equity price movements (business risk) with a Merton-type model.

The model has a strong theoretical background and provides a good basis for credit management of broadly diversified portfolios (global database of about 42,000 listed companies and 74,000 corporate bonds) – even compared to an army of credit analysts without real portfolio responsibility. We have been working with Credit Edge for over 20 years and are among the most experienced users in the market.

What it means:

- We systematically use the model to:

- continuously and efficiently screen the entire universe for expensive and cheap bonds

- continuously monitor and quickly detect any changes in credit quality, both in the universe as a whole and in the portfolios

- individually analyse and compare sectors, regions and individual companies, both with each other and over time

- simulate possible changes in balance sheet and income structure, for example after an acquisition

Step 2 – Qualitative research, the basis for business analysis

What we do:

We complement the quantitative results of the analysis and screening process with qualitative information about the company so that we can better assess and understand the specific risks of a given company and the investment universe.

What it means:

- Company-specific factors, to be considered:

- Changes in credit quality

- Stability of management, market position, products, legal environment, bargaining power of suppliers, bargaining power of buyers, risk of substitution, risk of new entrants, sectoral competition

- Credit rating reports

- Regulatory and country risks

- Bond-specific factors, to be considered:

- Amount issued and amount outstanding, issue date (liquidity)

- Coupons, step-up coupons

- Call/put options, sinking funds

- Senior/subordinated debt, capital structure, guarantees

- Covenants

- Regulatory and fiscal rules

Step 3 – Construction of the portfolio, the basis for implementation

What we do:

Selection of specific bonds to build portfolios in line with the investment strategy, the risk budget and the investment guidelines.

We seek opportunities through active credit allocation, i.e. by selecting and weighting sectors, industries, rating categories and countries.

What it means:

- Based on the credit cycle, the economic cycle, central bank policies, current and historical valuations, etc., we define the following criteria:

- Underweighting or overweighting industries, countries, ratings, sectors, currencies, etc.

- Strict limits and rules on individual positions and issuers (diversification is essential!)

- Selection of securities based on quantitative and qualitative analyses and corresponding weighting in the portfolio

- Furthermore, when building the portfolio, we apply the following strict principles:

- Rigorous active weighting of issuers, i.e. the lower the credit quality, the lower the active weighting

- Rigorous approach to spread sensitivity, i.e. the longer the duration, the lower the active weighting

- Careful consideration of transaction costs, an important factor in fixed income management